In April 2024, the China Securities Regulatory Commission ("CSRC") issued five cooperation measures with Hong Kong regarding the capital markets to support leading mainland companies to list in Hong Kong. In October 2024, the Securities and Futures Commission of Hong Kong ("SFC") and the Stock Exchange of Hong Kong Limited ("SEHK") issued the Joint Statement on Optimizing the Timetable of the Examination and Approval Process for New Listing Applications, which sets up a "fast examination and approval channel" for eligible A-share listed companies whose valuation is above RMB 10 billion. Under the support and guidance of relevant policies, since the second half of 2024, a large number of A-share listed companies have been preparing to issue H shares for listing in Hong Kong. As a special type of direct overseas issuance and listing by domestic enterprises, compared with H-share listing by ordinary domestic enterprises, A-share listed companies who issue H shares for listing are subject to dual A-share and H-share supervision. However, the efficiency and certainty of approval and listing for A-share listed companies is higher due to the fact that A-share listed companies already have a high level of standardization and a public market capitalization that can be referenced. This article focuses on the special legal issues involved in the issuance and listing of H shares in Hong Kong by A-share listed companies (for other articles in this series, please refer to 《境外上市备案新时代系列(三) — 直接境外上市及全流通篇》《境外上市备案新时代系列(十一) — GDR篇》).

Listing of A-share listed companies in Hong Kong after implementation of the filing system

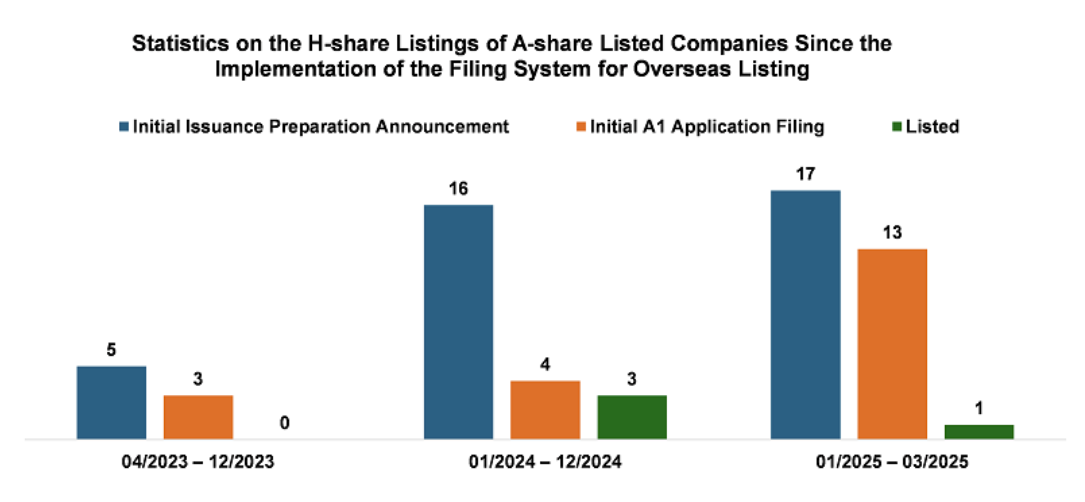

According to statistics, since the implementation of the filing system for overseas listing for domestic enterprises until March 31, 2025, a total of 38 A-share listed companies have announced preparations for initial public offerings of overseas listed foreign capital shares (H shares). Among these, 20 A-share listed companies have submitted applications to the SEHK for issuing and listing H shares and four companies have completed the listing of H shares, as shown in the chart below. In the first quarter of 2025 alone, the number of H-share listed companies announcing their preparation for listing H shares exceeded that of 2024. Judging from the market's response, there will be a new round of A-share listed companies listing in Hong Kong in 2025.

Main procedures

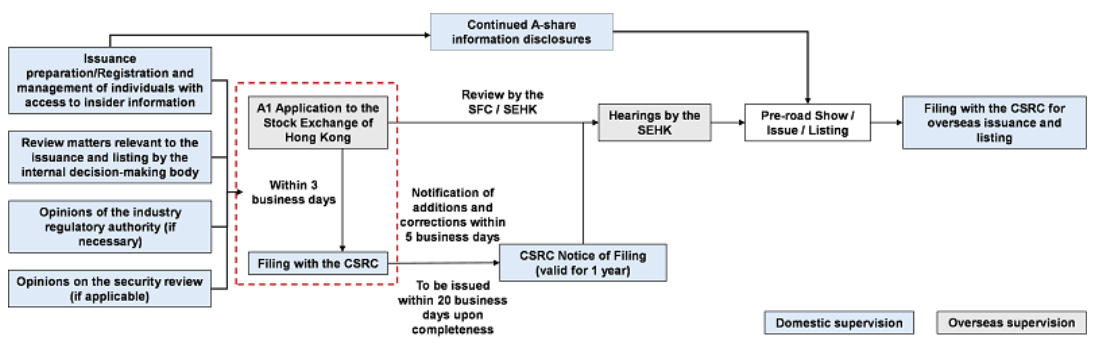

A-share listed companies that apply to issue overseas listed foreign capital shares (H shares) and list on the SEHK are subject to the Trial Administrative Measures of Overseas Issuance and Listing of Securities by Domestic Companies and relevant supporting guidelines. CSRC has implemented a filing system for overseas listing of foreign capital shares (H shares). However, A-share listed companies do not issue additional shares as underlying securities as is the case in the issuance of Global Depository Receipts (GDRs); thus, their issuance and listing of H shares are not subject to review by the mainland stock exchange and CSRC registration procedures. In addition, A-share listed companies must also comply with information disclosure regulatory requirements for A-share listed companies during the issuance and listing of H shares. The main procedures for H-share listing of A-share listed companies are as follows.

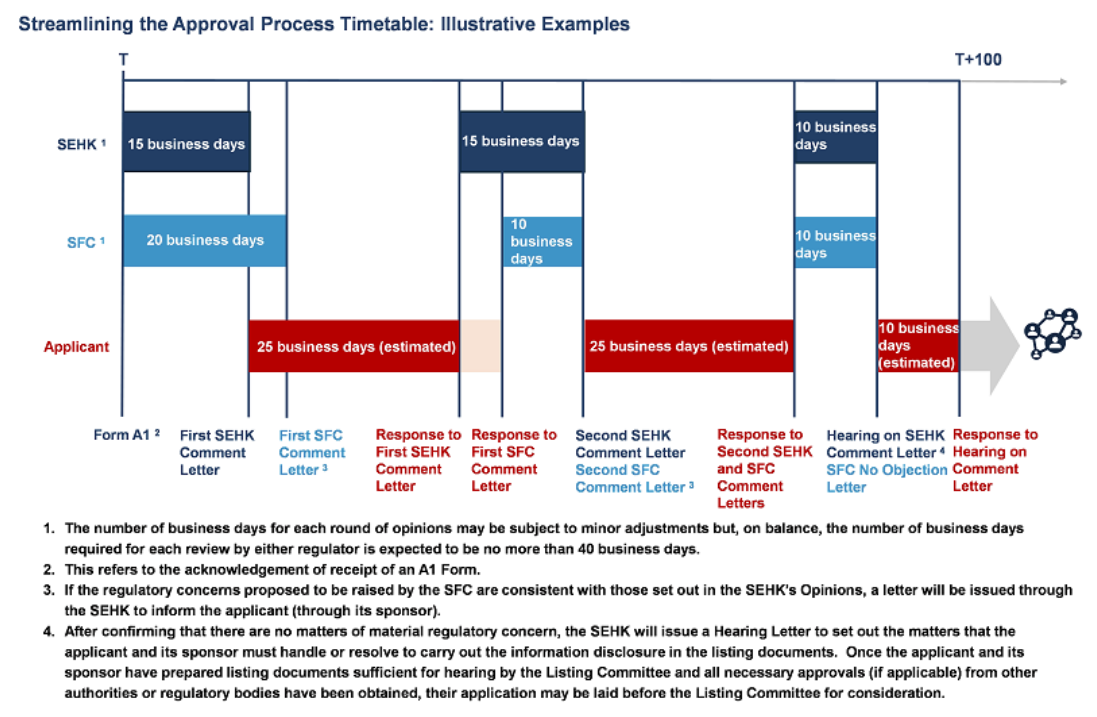

The H-share listing approval procedures for qualified A-share listed companies have been simplified following an October 2024 joint announcement by the SFC and the SEHK. Specifically, the SFC and the SEHK will undertake only one round of regulatory opinions and will complete their work in no more than 30 business days for those A-share listed company applicants that (1) have an estimated market capitalization of HK $10 billion or more; and (2) confirm, with a legal opinion, material compliance with A-share listing legal and regulatory requirements in the two full financial years prior to submitting the H-share listing application submission. The SFC and SEHK examination and approval procedures are as follows.

Foreign investment access

When preparing for an H-share listing, an A-share listed company should examine whether the specific businesses in which the company and its subsidiaries engage are within the scope of industries prohibited or restricted for foreign investment as stipulated in the Special Administrative Measures (Negative List) for Access of Foreign Investment; and, if so, what impact that an H-share issuance would have on those businesses and possible countermeasures. For example, if an A-share listed company or its subsidiaries operate the value-added telecommunications business, the H-share issuance plan may be determined by taking into account the foreign investment status of the top ten shareholders of the listed company, percentage of H shares to be issued, equity structure, specific business type, and other factors. An A-share listed company must obtain approval from the relevant authorities if it intends to issue H shares and operates within an industry prohibited to foreign investment as stipulated in the Special Administrative Measures (Negative List) for Access of Foreign Investment. Foreign investors may not participate in the operation and management of such enterprises, and their shareholding percentage must be determined with reference to the relevant provisions on the administration of domestic securities investment by foreign investors.

We observe that top priority during the H-share filing approval process is given to each applicant’s continuous multi-dimensional regulation and supervision of equity, business, operation and management, and compliance, etc., based on our comprehensive analysis of public market cases since the implementation of the overseas listing filing system for domestic enterprises. In practice, operators from different industries may have different solutions when dealing with specific issues. We have also had meaningful success in our practice by combining different technical solutions in projects in specific industries and look forward to exploring technical solutions with market participants.

Management of insider information

For an A-share listed company, preparing for the issuance and listing of H shares is considered insider information. This requires A-share listed company applicants to observe the following during the preparation and application process:

(1) before publicly disclosing insider information in accordance with the law, the company must, in accordance with the relevant provisions, prepare files of the individuals with access to the company's insider information, timely record the names of those with access to the insider information in the stages of discussion, preparation, debate and consultation, and conclusion of contracts and at the stages of reporting, transmission, compilation, resolution and disclosure, and provide the time, places, evidence, methods and contents of the insider information, and those individuals with access to the insider information must confirm the same;

(2) the listed company must prepare a memorandum on the progress of a material event, the contents of which includes but is not limited to the time of each key point in the course of preparation and decision-making, the names of the individuals who participate in the preparation and decision-making, the manner of preparation and decision-making, etc.

The A-share listed company applicant should urge the relevant people involved in the memorandum for the progress of a material event to sign on the memorandum for confirmation. Meanwhile, the listed company will need to sign a confidentiality agreement with the relevant participants and notify them of prohibition of disclosure of insider information and prohibition of insider trading. In practice, an A-share listed company applicant may first choose the right time to publish an announcement on researching and demonstrating a material event, or convene a board meeting to deliberate and publish an indicative announcement on authorizing the management to initiate the preparatory work for the issuance and listing of H shares, and appropriately avoid the risk of disclosure of insider information and insider trading by disclosing information in a timely manner.

Information disclosure

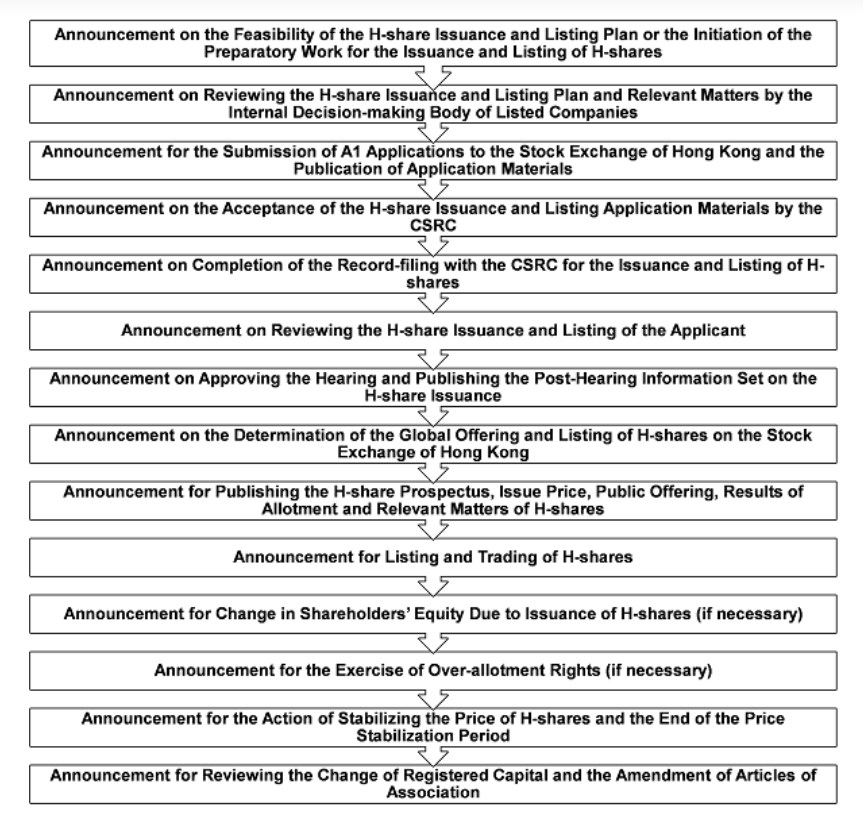

I. A-share information disclosures during the H-share listing process

An A-share listed company generally makes the following information disclosures when applying to issue and list H shares:

II. Continued information disclosure in both locations after dual listing

After completing the listing of A + H shares, a listed company should continue to meet both A-share and H-share information disclosure requirements, and H-share announcements are required to be prepared in both Chinese and English. Both A-share and H-share listings stipulate simultaneous information disclosure rules, i.e., a listed company releases any information to any stock exchange where its securities are listed and also needs to concurrently disclose relevant information on other stock exchanges.

Corporate governance

During the H-share issuance and listing process, an A-share listed company will formulate internal governance rules such as the draft articles of association, which conform to the SEHK listing rules, the Code of Business Administration, and other matters. In addition to the A-share corporate governance requirements, the main special governance requirements to be noted are:

(1) Determining the role of board members and the composition of the board, which must include executive directors, non-executive directors and at least three independent non-executive directors (i.e. independent directors), at least one of the independent directors habitually resides in Hong Kong;

(2) The board cannot be composed of members of a single gender;

(3) There must be at least two executive directors who habitually reside in Hong Kong. Subject to certain conditions, the SEHK will generally provide an exemption from this requirement for A-share listed companies without significant business operations in Hong Kong;

(4) The role of board chairman and chief executive officer should be undertaken by two separate individuals, but the dual chairman-chief executive role can be justified by explaining its importance to the company's business (e.g., the founder);

(5) One person (with relevant qualifications or experience required in Hong Kong) must be appointed as the company's secretary in order to assist the listed company and its directors to comply with the SEHK listing rules and other applicable Hong Kong laws and regulations;

(6) The board of directors must set up an audit committee, a nomination committee, and a remuneration and appraisal committee. The nomination committee is chaired by the chairman of the board of directors or an independent director (and at least one member must be of a different gender), while the remuneration and appraisal committee and the audit committee must be chaired by an independent director.

In addition, to implement the revised PRC Company Law, the CSRC issued the revised Guidelines for the Articles of Association of Listed Companies and other rules on March 28, 2025. In combination with the adjustments and transition period arrangements previously issued by the CSRC, an A-share listed company needs to adjust its corporate governance structure prior to January 1, 2026. The company's articles of association stipulate that an audit committee shall be established in the board of directors, which exercises the functions and powers of the supervisory board as prescribed by the Company Law and has no supervisory board or supervisor. An A-share listed company preparing for an H-share issuance and listing may consider amending and adjusting its corporate governance structure, articles of association, other procedural rules and the applicable articles of association after the H-share issuance and listing in accordance with such requirements.

Requirements as to the number of shares held by the public and the scale of issuance

According to the SEHK listing rules, when an A-share listed company issues H shares, the total number of A shares and H shares held by the public must account for at least 25% of the total amount of the issuer's issued shares, and the H shares may not be less than 15% of the total amount of the issuer's issued shares. If the market capitalization of the listed company exceeds HK$ 10 billion, it may apply to the SEHK for an issuance ratio of 15% – 25% of its shares held by the public; if it wishes to issue less than 15% of its shares, it needs to communicate on a case-by-case basis and apply for an exemption. According to statistics, from 2020 to 2023, there were eight A-share listed companies that issue H shares on the SEHK Main Board, among which four A-share listed companies were exempted from the minimum 15% shareholding ratio and were allowed to issue H shares accounting for 5% – 12.5% of their total amount of issued shares.

The H-share issuance ratio and the number of publicly held shares are proposed to be changed, according to a consultation document published by the SEHK on December 19, 2024. The document provides that H shares to be listed on the SEHK must account for at least 10% of the total number of the category of H shares (i.e., A shares and H shares) at the time of listing, or the expected market value of H shares at the time of listing is at least HK$ 3 billion, and the number of publicly held A shares will no longer be included in calculating the number of publicly held H shares, and the threshold for the number of publicly held shares is the same as the above requirements. The consultation document is open for public comments until March 19, 2025. If this policy is implemented, A-share listed companies with an expected market value of more than HK $30 billion may see a significant reduction in the issuance ratio requirement for their H shares. For other A-share listed companies with an expected market value of less than HK $30 billion, their issue ratio may also be reduced to 10%, which is helpful for A-share listed companies to balance the pressure of the price differential between the SEHK and the mainland exchange on which the A-share listed company is listed.

Notably, during the H-share listing process, the total capital stock of an A-share listed companies may change due to the grant of restricted shares, exercise of stock options, and the repurchase and cancellation of shares, which may also require the listed company to update the disclosure in its prospectus and calculation of the issuance ratio accordingly.

Lock-up period

According to the SEHK listing rules, the person or group of persons who are listed as controlling shareholders of an issuer in the H-share listing documents are not allowed to transfer their shares in the issuer within 6 months from the listing date. And, within 6 months after the expiration of the lock-up period, the person or group of persons who are listed as controlling shareholders of an issuer may not sell any of the issuer's securities to the extent they would lose their status as controlling shareholders. Therefore, A-share listed company shareholders face no additional lock-up period due to the issuance of H shares other than that applicable to the controlling shareholders.

Capital raised

When raising funds by issuing H shares, A-share listed companies are not restricted by issuance ratios, financing intervals, or top-up ratios, and their financing plans may be more flexible. In terms of the use of the raised funds, according to the relevant SAFE regulations and its latest guidance, in principle, listed companies must, handle the overseas listing registration with the competent mainland foreign exchange bureau within 15 business days after the completion of the initial public offering or over-allotment and receive a registration certificate. In principle, the raised funds should be repatriated in a timely manner in RMB or foreign currency, and the use of the raised funds should be consistent with the contents listed in the prospectus, resolutions of the board of directors or the shareholders' general meetings, and other publicly disclosed documents. After communicating with and obtaining the consent of the SAFE, the raised funds may also be retained and invested overseas or be used to carry out relevant business in compliance with the relevant foreign exchange control regulations.

Conclusion

Since the implementation two years ago of the Trial Administrative Measures of Overseas Issuance and Listing of Securities by Domestic Companies, positive progress has been made in the record-filing administration for overseas listings. Under the background of the continuous implementation of the "five preferential treatments for Hong Kong" capital markets policy and support given to Hong Kong to consolidate and enhance its status as an international financial center, it is expected that more domestic A-share listed companies will seize the opportunity to make better use of the international capital markets, optimize their capital structure and shareholder composition, diversify financing channels, enhance their global brand awareness and competitiveness, and prepare for their long-term development.

Important Announcement

This Legal Commentary has been prepared for clients and professional associates of Han Kun Law Offices. Whilst every effort has been made to ensure accuracy, no responsibility can be accepted for errors and omissions, however caused. The information contained in this publication should not be relied on as legal advice and should not be regarded as a substitute for detailed advice in individual cases.

If you have any questions regarding this publication, please contact:

Zhenyu WANG

Tel: +86 10 8516 4106

Email: zhenyu.wang@hankunlaw.com